I’ve had my 2023 XSE Hybrid for about two years now and I’m nearly halfway done with the payments. My minimum is $865 a month, but I usually pay $1,000 to $1,500 when I can. I wanted to refinance, but it looks like Toyota doesn’t let you do that? Has anyone here dealt with this? How did you handle refinancing, and do you know any good credit unions that accept new customers with a car that’s halfway paid off? I have great credit and just want to pay it off faster.

One more thing—when I make a payment towards the principal only, the next bill says I’m past due. Why is that? Are principal-only payments not allowed anymore?

You probably won’t be able to get a better rate by refinancing. Rates for used cars are usually worse than for new ones. Just keep throwing extra money at the principal.

You’re getting marked as past due because you’re skipping the interest portion. You still have to make the regular monthly payment, then anything extra can go to the principal.

John said: @vinic

I tried refinancing my 2-year-old car and barely saw a difference in the rate. Wasn’t really worth it in the end.

Yeah, on a car that’s already a couple years old, a 1% drop won’t do much. You’re usually better off keeping the rate and just throwing more money at the loan early on.

@vinic

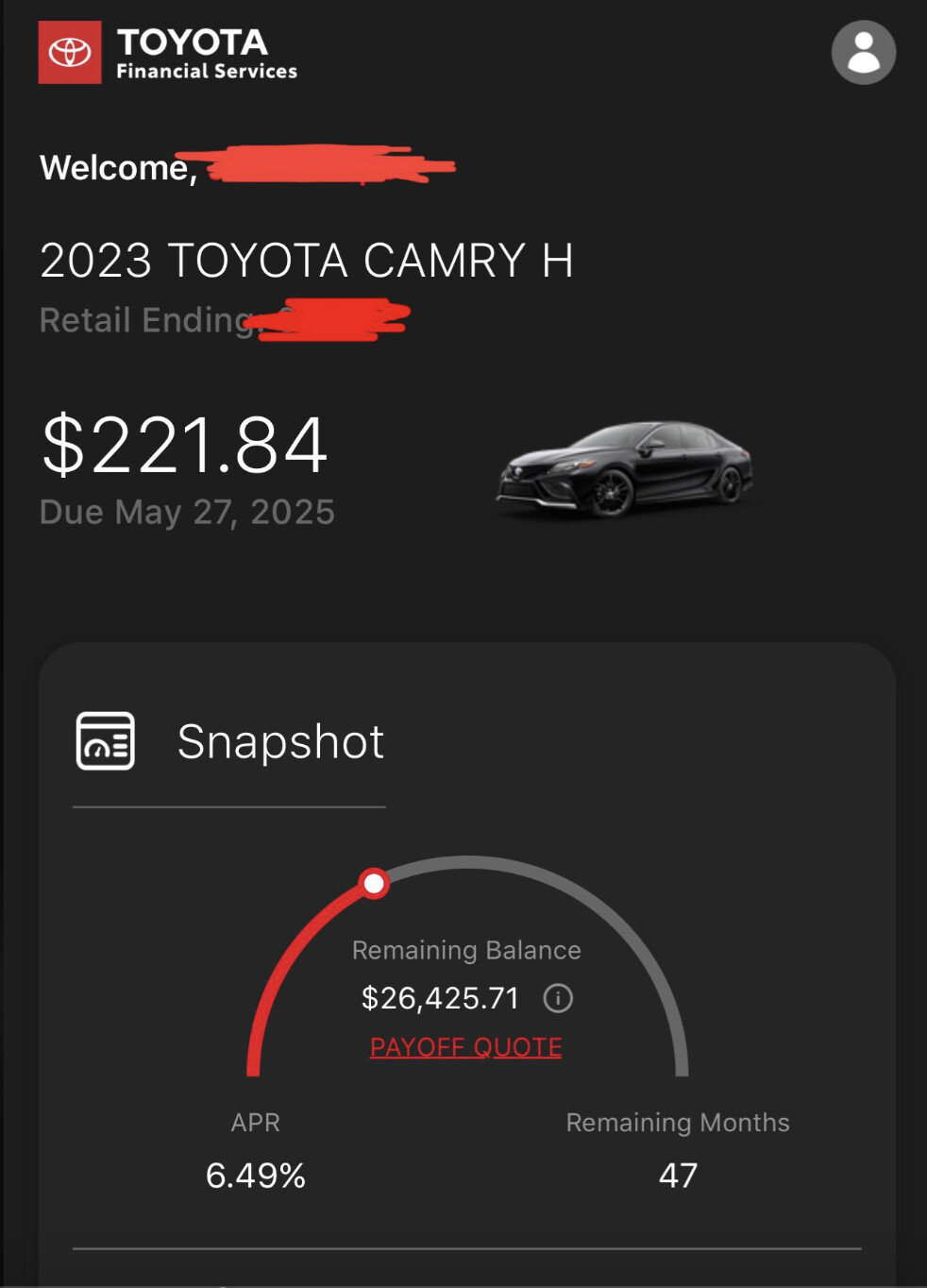

I just refinanced and got 6.49%. The best deal I saw was 5.64% but I didn’t qualify for that one yet. Still, 6.49% isn’t too bad right now. I wouldn’t refinance unless your current rate is really high.

Making a ‘principal only’ payment doesn’t replace your normal monthly payment. It’s just extra to help pay off the loan faster. I split my car payment in half every two weeks and also make one principal-only payment monthly. I still follow my bi-weekly schedule. The extra principal payments help reduce the overall loan amount and speed things up.

I’ve had my Camry for just over a year with Toyota’s financing, and it was almost 10%. When I got my tax refund, I refinanced through a local credit union and dropped it to 5% APR, plus lowered my monthly payment by $100.

Check local credit unions online and compare their rates. With good credit, you should be fine getting approved.